By: Sean Gallagher, CFP®

What is the Federal Funds Rate?

The federal funds rate is the overnight rate charged between banks to lend their reserves back and forth. While this rate does not directly impact consumer or businesses loans, increased rates that the banks must pay to meet their reserve requirements cause them to pass their costs onto the consumer or business in higher lending rates.

Changes to the federal funds rate will influence most consumer and business borrowing costs, including rates on mortgages, credit cards, savings accounts, car loans, and corporate debt.

Why Does the Federal Open Market Committee Change the Federal Funds Rate?

The FOMC changes rates when they are trying to slow down or speed up the economy's growth. Increasing the federal funds rate will raise short-term rates, effectively reducing the supply of money in the economy by making it more expensive for consumers and businesses to borrow money.

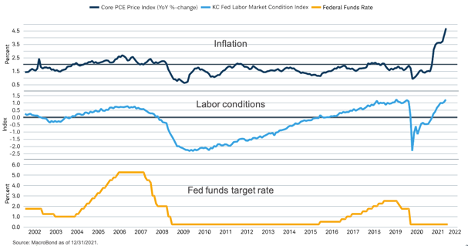

As you can see in the chart below from MacroBond, the federal funds' target rate has historically followed rising inflation and labor conditions quite closely.

How are Fixed Income Asset Classes Affected by Changes in the Federal Funds Rate?

Short-term credit typically performs better than longer-term credit in the fixed income market during rising interest rate environments.

Bond prices are inversely related to interest rate changes, meaning as rates rise, existing bond prices fall and become less valuable. Longer-duration bonds come with greater maturity risk considering there is more uncertainty about where interest rates will be in the future when the bond matures.

The following chart from Goldman Sachs Asset Management shows how different fixed income asset classes have fared during four fed interest rate increase cycles.

While some of these results may not be ideal returns for fixed income, it's essential to keep in mind the purpose of fixed income in a diversified portfolio. Bonds are ballast in the portfolio that provides stability and reduced volatility from the equity market. Abandoning fixed income in a portfolio can result in a much bumpier ride for an investor.

Rising interest rates make it more costly for businesses to borrow money to fund their operations and support growth.

How Do Rising Rates Impact Market Returns?

Intuitively, one would think that this would dampen equity market returns during these periods. The initial announcement of raising interest rates typically offers a "shock" to equity markets and often results in a slight pullback.

With that said, the chart below from Haver Analytics and Goldman Sachs Asset Management shows that overall returns of the US market during these cycles are much in line with the long-term average. The average S&P 500 annualized return over the last six fed hiking cycles is 9.5%, not far behind the index's long-term average return of around 10.5%.

While rising interest rates are intended to slow down economic growth, they do not signal an urgent need for change in investment policy. At HIGHLAND, we constantly monitor client portfolios to ensure they are positioned to weather investment risk in the ever-changing economic landscape.

Sean Gallagher is a CERTIFIED FINANCIAL PLANNER™ at HIGHLAND Financial Advisors, a Fee-Only financial planning firm that offers comprehensive financial planning, retirement planning, and investment management. Sean graduated from Virginia Tech’s financial planning program in 2018 and successfully passed the CFP® national exam in 2019. As a Financial Planner at HIGHLAND Financial Advisors, Sean works on developing comprehensive financial plans and investment management for all clients.